In the last post I looked at how much of your pay check goes into national insurance and tax both in absolute value and percentage. In this post I look at how much it is possible to claim in tax credits and how this would have changed under the now scrapped cuts proposed in the summer. The tax credit system as a whole is pretty complicated and there are many rules and regulations about who can claim etc. There are also added complications when situations change during a year, for example due to change in earnings or birth of a child. I will not look at the complicated edge cases but rather some simple situations so that trends can be seen.

I am also not in any way an expert in taxes, in fact I have spend the vast majority of my life in education and therefore not paying any tax. Furthermore even though I currently have a job and pay tax it is in Germany, so I have no first hand experience. This study is purely for curiosity's sake. To accurately calculate your own claim to tax credits please use one of the online calculators, e.g. the government and monesavingexpert.

My examples will be situations where both working tax credits and child tax credits are eligible, the rules for which I am taking from Which's website because they give clear lists and good discussions of all the rules. The working tax credits (WTC) are:

The child tax credits (CTC) are:

Then the taper rate is 41%. This means the amount possible to claim is reduced by 41p for every £1 over the threshold of £6,420.00 per year before taxes and national insurance. They say that the order in which the money is taken away is:

It's not clear why this matters as the order in which the claim is taken away doesn't affect the amount of money received as far as I can tell. The websites revenue benefits and tax guide for students give nice worked examples of tax credit claims.

The proposals for the cuts to tax credits were (I couldn't find any official list of the changes, but the major newspapers seemed to agree on the details):

This isn't quite the end of the changes, it has been proposed that the country adopt the national living wage. This is in effect a raise of the minimum wage from £6.50 to £7.85 (£9.15 in London). There will also be an increase in the tax free allowance to £11,000.

Rather than calculate a few examples by hand I wrote a function in Julia to calculate the tax credit claim given the income and number of children etc. This means that the computer can sweep across a range of incomes and see what can be claimed. This is much the same as in the first part.

The first example is someone with no children. There is no real change to the maximum possible tax credits as they are not eligible for the family or child elements. The taper is the clear difference, the extra money from the tax free allowance not making much difference.

The second example is a lone parent with two children claiming the full £300 a week for childcare for the whole year. This is a limiting case as the chances are a parent would want to be on holiday with their children and therefore not claim childcare for those weeks. Again the taper rate and the lower wage that the taper starts is the biggest difference. This does highlight the fact that WTC and CTC are not just for people on low incomes. It is still possible to claim when you earn almost £60k, however this would be significantly reduced under the proposed cuts.

These graphs do not take into consideration the increase in minimum wage as they are a sum of yearly income. The rules described above can be rewritten in terms of weekly earnings as described in revenue benefits. The increase in minimum wage is expressed as all those earning below £7.85 now earning exactly that much. This is again a limiting case as the chances are that those earning slightly more than £7.85 now will have their wage increased to highlight the fact they were earning more than minimum wage before. The yearly wage is calculated assuming a 40 hour working week and 28 days of holiday including bank holidays.

The person without children no longer receives any tax credits under the proposals. This is the aim of the living wage; that it is sufficient to live off without the government having to intervene.

The lone parent with two children and childcare does not receive enough from the increased minimum wage and tax free allowance to recoup the losses due to tax credit cuts at any wage.

The conclusion to me from playing around with the tax credit changes is that in the simple cases that I looked at the tax credit cuts amount to a cut in tax credits with very few people better off as a result. There may well be some specific cases where this is not true when all of the rules are put into place.

I have added the code to my GitHub so if there is anyone out there who wants to play around with this they can. The function "run_tax.jl" imports all of the functions and produces the data used in the graphs and more, exporting to a .txt file. These can then be imported into XMGrace or Excel etc to make the graphs. Feel free to fork and edit.

Oh, and happy new year!

I am also not in any way an expert in taxes, in fact I have spend the vast majority of my life in education and therefore not paying any tax. Furthermore even though I currently have a job and pay tax it is in Germany, so I have no first hand experience. This study is purely for curiosity's sake. To accurately calculate your own claim to tax credits please use one of the online calculators, e.g. the government and monesavingexpert.

My examples will be situations where both working tax credits and child tax credits are eligible, the rules for which I am taking from Which's website because they give clear lists and good discussions of all the rules. The working tax credits (WTC) are:

- Basic element (one per single claimant or couple) - £1,960,

- Couples’ and lone parents’ element - £2,010,

- 30 hour element (only one element allowed per couple) - £810,

- Disabled worker element - £2,970,

- Severe disability element - £1,275,

- Childcare element for one child - 70% of cost to a maximum of £175 a week,

- Childcare element for two or more children - 70% of cost of childcare to a maximum of £300 a week.

The child tax credits (CTC) are:

- Family element (one or more children) - £545,

- Child element (one for each child or young person) - £2,780,

- Disability element (one for each child) - £3,140,

- Severe disability element (one for each child) - £1,275.

Then the taper rate is 41%. This means the amount possible to claim is reduced by 41p for every £1 over the threshold of £6,420.00 per year before taxes and national insurance. They say that the order in which the money is taken away is:

- WTC without childcare,

- WTC childcare,

- Child parts of CTC,

- Family part of CTC.

It's not clear why this matters as the order in which the claim is taken away doesn't affect the amount of money received as far as I can tell. The websites revenue benefits and tax guide for students give nice worked examples of tax credit claims.

The proposals for the cuts to tax credits were (I couldn't find any official list of the changes, but the major newspapers seemed to agree on the details):

- The threshold before the taper starts is cut to £3,850,

- The taper rate increased to 48%,

- The family element is removed,

- The child element is only for the first 2 children.

This isn't quite the end of the changes, it has been proposed that the country adopt the national living wage. This is in effect a raise of the minimum wage from £6.50 to £7.85 (£9.15 in London). There will also be an increase in the tax free allowance to £11,000.

Rather than calculate a few examples by hand I wrote a function in Julia to calculate the tax credit claim given the income and number of children etc. This means that the computer can sweep across a range of incomes and see what can be claimed. This is much the same as in the first part.

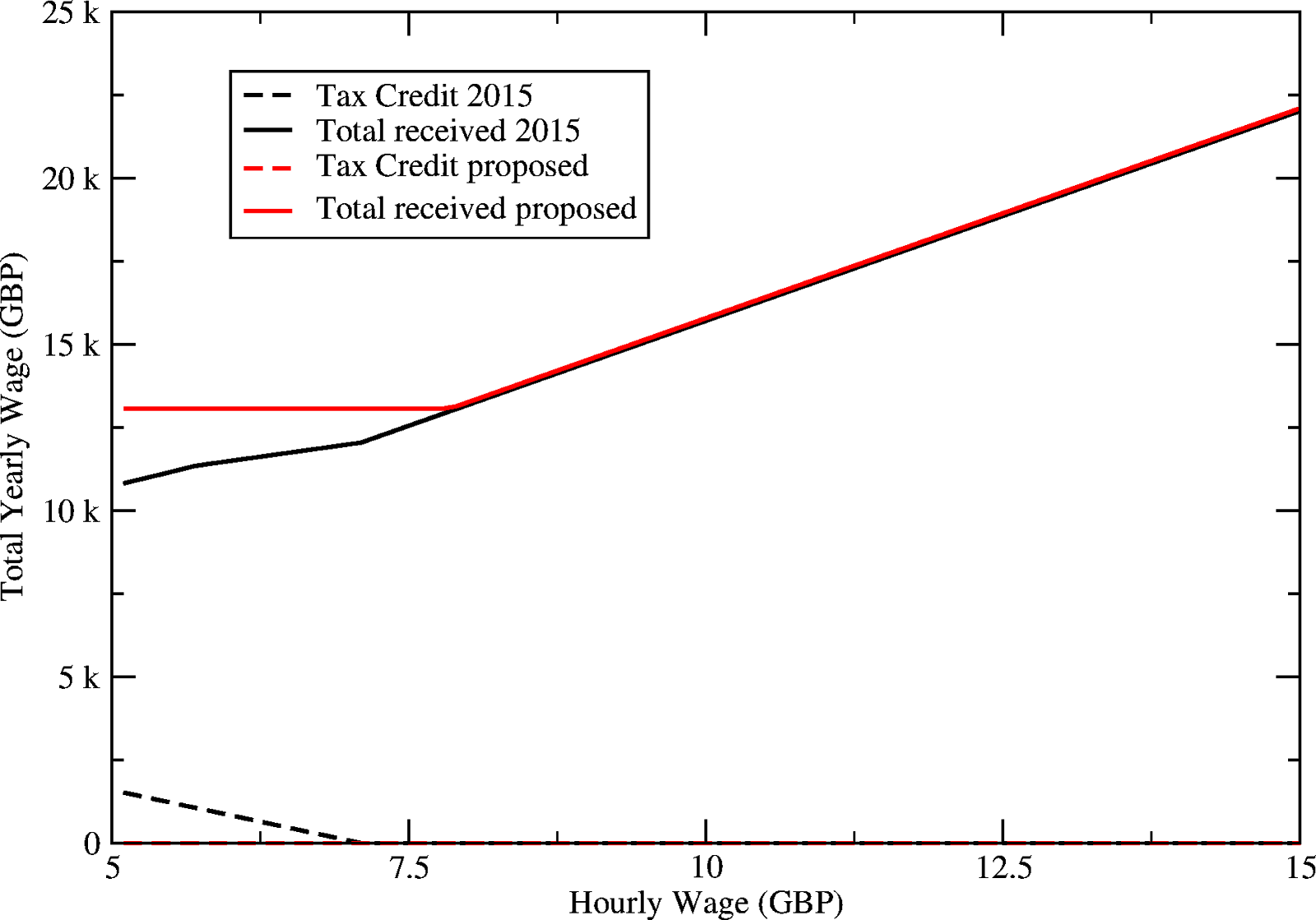

The first example is someone with no children. There is no real change to the maximum possible tax credits as they are not eligible for the family or child elements. The taper is the clear difference, the extra money from the tax free allowance not making much difference.

|

| WTC received for someone with no children. |

The second example is a lone parent with two children claiming the full £300 a week for childcare for the whole year. This is a limiting case as the chances are a parent would want to be on holiday with their children and therefore not claim childcare for those weeks. Again the taper rate and the lower wage that the taper starts is the biggest difference. This does highlight the fact that WTC and CTC are not just for people on low incomes. It is still possible to claim when you earn almost £60k, however this would be significantly reduced under the proposed cuts.

|

| WTC and CTC for a lone parent with two children claiming the full £300 per week in childcare |

The person without children no longer receives any tax credits under the proposals. This is the aim of the living wage; that it is sufficient to live off without the government having to intervene.

|

| WTC received for someone without children expressed in terms of hourly wage |

|

| WTC and CTC for a lone parent with two children claiming the full £300 per week in childcare in terms of hourly wage |

I have added the code to my GitHub so if there is anyone out there who wants to play around with this they can. The function "run_tax.jl" imports all of the functions and produces the data used in the graphs and more, exporting to a .txt file. These can then be imported into XMGrace or Excel etc to make the graphs. Feel free to fork and edit.

Oh, and happy new year!

Comments

Post a Comment